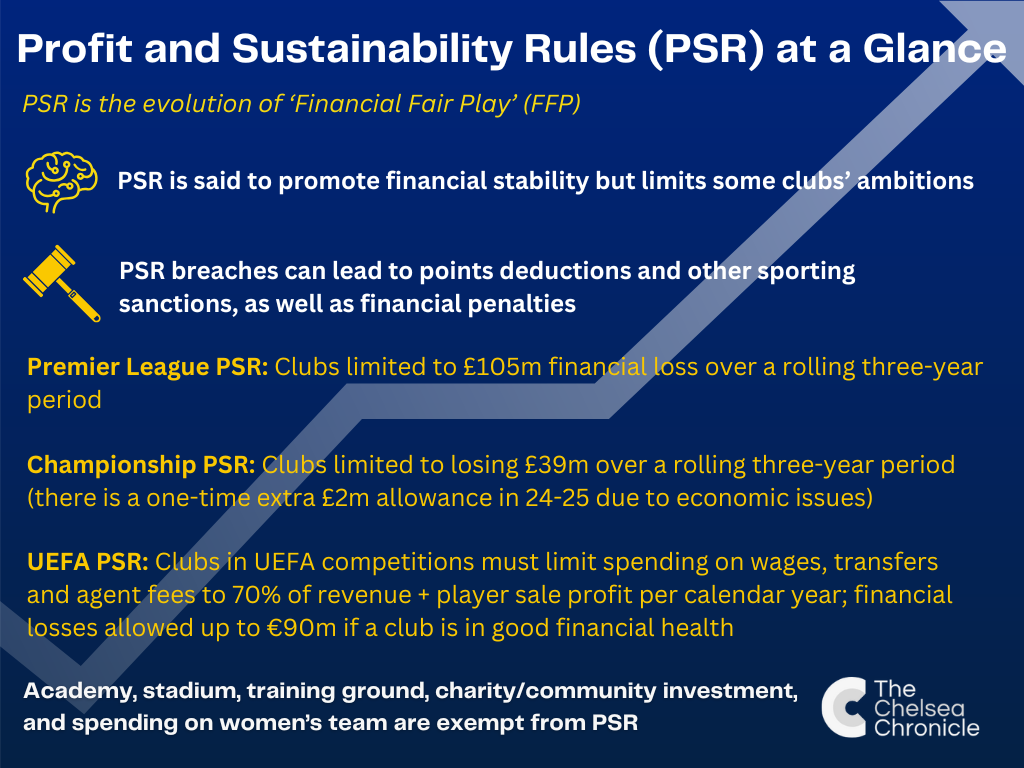

Chelsea have short-circuited the Premier League’s system of Profit and Sustainability Rules – or ‘Financial Fair Play’, in old money – through a series of innovative accounting techniques.

At this stage, this jiggery-pokery is well document. Chelsea have sold two hotels, a car park and a portion of their training ground to themselves to create artificial profits in the books.

The sale of the women’s team to another BlueCo-owned company via the same method has raised £200m, although it has only been provisionally cleared by the Premier League, who are assessing the deal under their Fair Market Value criteria. That may be why Chelsea are also considering a minority stake in the women’s team to an external investor, i.e., to justify the £200m price tag.

This financial trickery won’t balance the books forever, though. Indeed, as far as UEFA, who have their own Financial Fair Play criteria, are concerned, the chicanery isn’t working.

Chelsea are expected to fall short of European football’s governing body’s standards, which include a calendar-year 70 per cent squad-cost-to-turnover cap and a maximum three-season loss limit of around £75m. Next term, given that Chelsea will probably have European football of some description season, Chelsea will be at risk of a further UEFA breach.

That will probably come with a financial penalty, which Todd Boehly and Clearlake Capital will accept as a necessary cost of building Enzo Maresca’s squad.

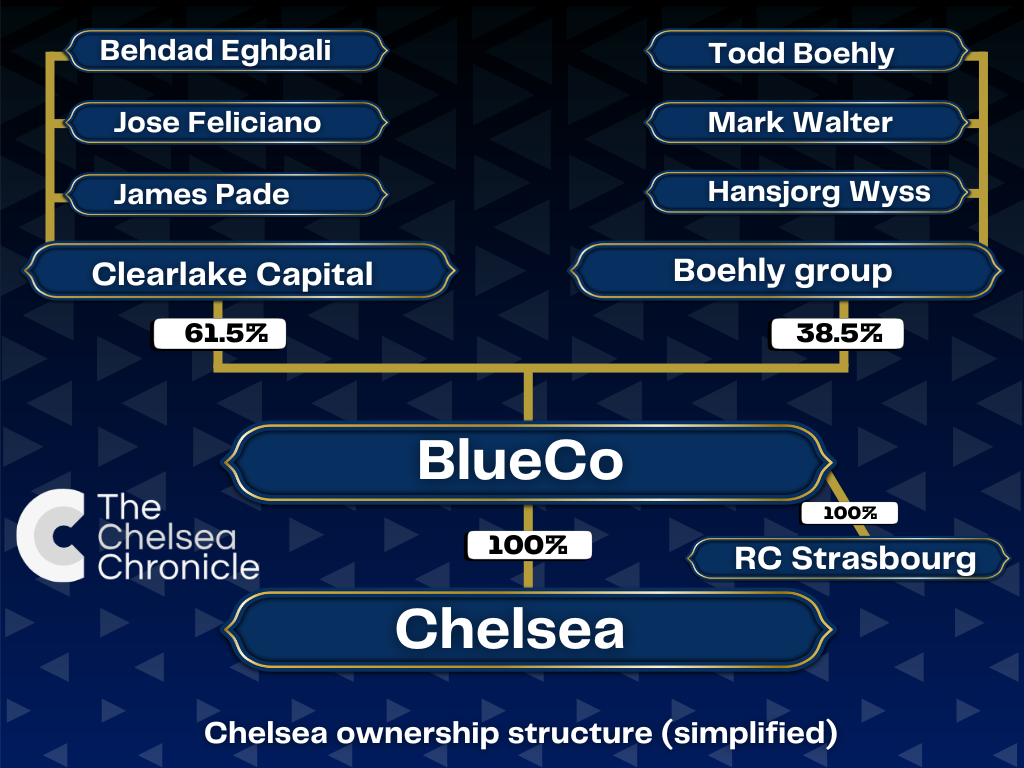

The BlueCo consortium has certainly come at football club ownership from the left field. The various football finance experts The Chelsea Chronicle speaks to say the private equity billionaires are either visionary disruptors or have fundamentally misunderstood how the game works – very few are on the fence when it comes to Chelsea’s owners.

Everyone knows how much the Blues have spent since the end of the Roman Abramovich era in May 2022, but what is equally jaw-dropping is the volume and mechanics of the transactions in and out of Stamford Bridge.

- READ MORE: £130m stadium naming rights deal already done as Chelsea offered Stamford Bridge replacement

Chelsea’s contract strategy analysed by Kieran Maguire

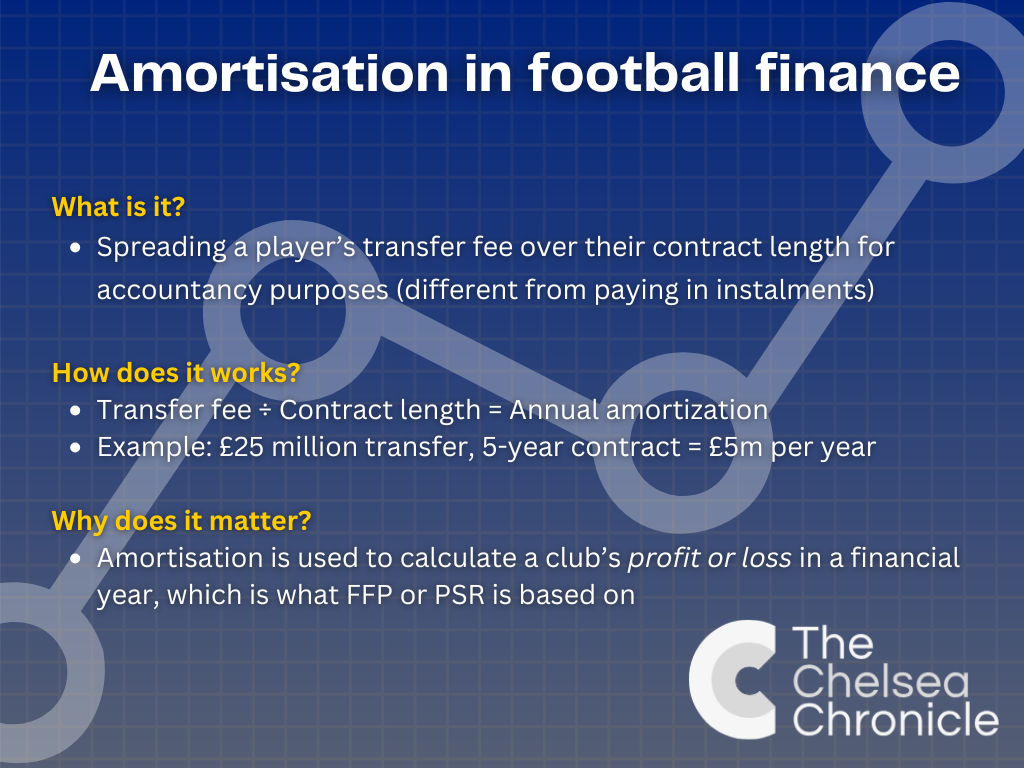

Famously, Chelsea started to sign players on ultra-long contracts as soon as Boehly and Clearlake arrived at the club.

The motivation was two-fold. By having long-term deals, you protect player market value and foster buy-in from young players for what is clearly not a win-now project.

Secondly, by having a player tied for seven, eight years or even nine, you are able to amortise his book value over a longer period of time. That’s useful because PSR and FFP are based on annual amortisation, not how much a player costs up front. The longer a contract, the smaller impact on the bottom line from year to year.

In the end, both the Premier League and UEFA changed the rules so that the maximum period over which a player’s book value could be amortised is now five years.

But Chelsea have persisted with the long contracts, showing that it was a definite market strategy as opposed solely to a PSR dodge.

This contract structure, as well as the sheer number of transfers in and out of the club has seen Chelsea shell out more than any other club in agents’ fees in recent year – an eye-watering £178m since the takeover, with £60m of that coming this season.

“I think Chelsea’s strategy is potentially high risk,” says University of Liverpool football finance lecturer Kieran Maguire, speaking exclusively to The Chelsea Chronicle.

“For every Cole Palmer they can cash in on in future years if they decide to part ways, there is a Mykhailo Mudryk or a Robert Sanchez.

“The downside of this strategy is that if you’re selling players, your profit on disposal is sales proceeds minus the player’s book value at the point of sale. The book value is the original cost minus amortisation. If you’re amortising the players over a longer period then the book value goes down slower, so the gains on player sales are that much lower.

“Having said that, the changes in the rule book for both UEFA and the Premier League mean that the PSR profit on disposal is a different figure to the one that appears in the accounts. This only applies to transactions after 31 July 2023, so this strategy works until it doesn’t work.

“I think they have done absolutely nothing wrong and, personally, I wouldn’t have changed the rules. I don’t think it’s a loophole; I think it’s a business risk. They just have a different approach to risk.”

- READ MORE: Potential crisis for Enzo Maresca as crucial Chelsea player is not happy with the manager’s tactics

Club World Cup finance blow for Chelsea

The Club World Cup this summer could be a salvation of sorts as far as PSR is concerned, with prize money of up to £97m up for grabs for Chelsea and Manchester City. At minimum, the Blues will bank £30m just for showing up, before performance-related bonuses.

Or at least, that was the amount that FIFA were advertising – and, presumably, the amount that Chelsea have budgeted for too.

However, the US government is set to charge tax on the prize money as things stand.

As well as the federal system tax varies from state to state, while there also complications around double taxation treaties, which might see clubs taxed both in the US and domestically.

In a worst-case scenario, Chelsea could lose up to 40 per cent of their prize money to the taxman, though FIFA are in talks with the US government to try and find a solution.

Receive a digest of our best Chelsea content each week direct to your mailbox