In a recent media outing, Chelsea co-owner Todd Boehly said something illuminating about his style: “When you own intellectual property like us, you’re only limited by your creativity as to where it goes.”

In football, intellectual property (IP) is business speak for, in this case, Chelsea’s brand, their image rights and the license to use the badge to sell products, services and experiences.

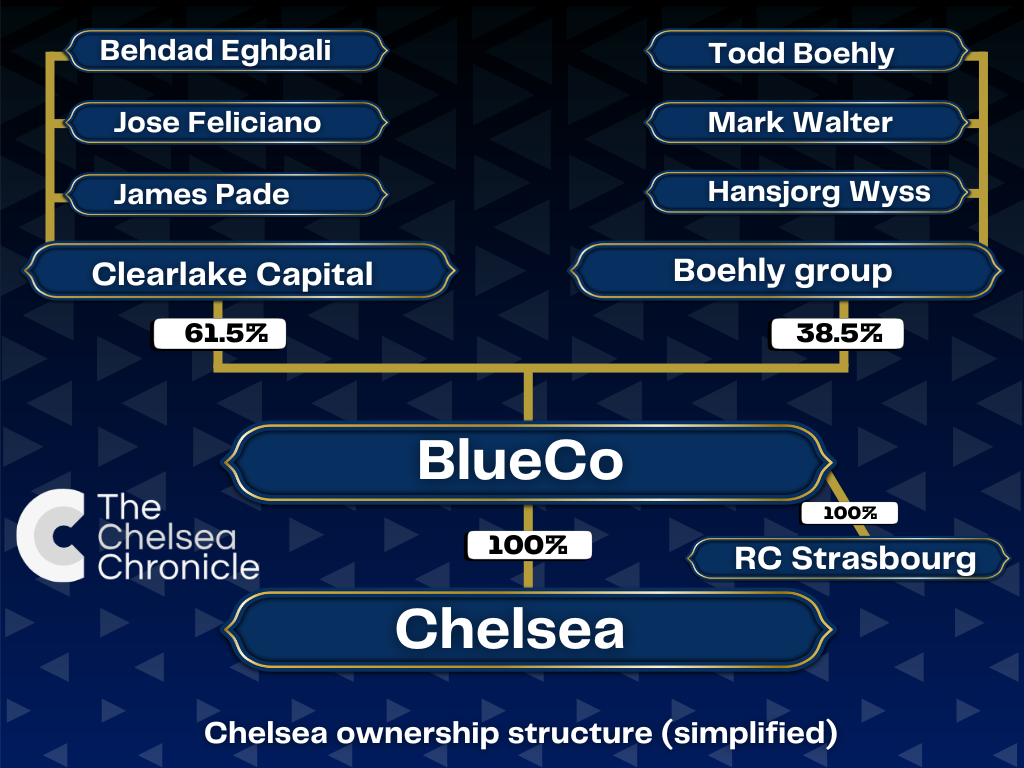

That IP is the reason that Todd Boehly, alongside Behdad Eghbali’s Clearlake Capital and a handful of other giants in the world of sports investment, spent to £2.5bn to take over Chelsea.

On paper, Chelsea look like a money pit. They’ve lost £367m in the last three published financial years – and we don’t even have 2023-24’s figures yet, which will likely show an operating loss of over £250m.

If the business isn’t making anywhere near enough money to cover costs, it falls on Chelsea’s owners to underwrite those losses via equity or loans, with the Clearlake-Boehly regime favouring the former.

Last week, there was another share issue, which is a mechanism through which the owners inject money into a business via the equity structure. It cost Boehly and Clearlake £65m.

The owners have plunged nearly £350m into the club this way in the last 12 months alone. They have also taken on third-party debt of £500m from Ares Management, on top of almost £500m in transfer debt.

Boehly, Eghbali, Mark Walter, Hansjorg Wyss and the rest of their colleagues in the crowded Chelsea corporate structure have also committed £1.75bn for the redevelopment of Stamford Bridge.

Basically, owning a club like Chelsea isn’t cheap – and how exactly the club’s financial backers ultimately plan to generate a return on their investment isn’t clear.

That said, Boehly, in the same interview with Bloomberg that touches on IP, insisted that “the industry is going to continue to go up in value.

“There is more revenue and attention coming in this direction, so it isn’t as if these valuations [of Premier League clubs and sports franchises in general] don’t make sense.

“They continue to make sense. There are very few [franchises], but they are the beating heart throughout the industry. Then, you have all these other industries developing around the beating heart.

“If the beating heart continues to go up in value, all the ancillary activity is going to continue to go up in value.”

But even massive success on the pitch in the Premier League and Champions League would barely make up the £200m-plus in operating losses that the Blues are currently posting each season.

So where is the value that Boehly – as well as dozens of other investors, especially from the United States private equity sphere – describes coming from, if it exists at all?

Could it be that the valuations of clubs like Chelsea are a speculative bubble that will burst if the markets conclude that prices have surpassed the inherent value of football teams as businesses?

Well, if Boehly’s record elsewhere is anything to go off, it’s unlikely that he’s backed the wrong horse.

Through Eldridge Industries, the 52-year-old is one of sport’s most successful investors and an almost deified figure within the industry.

| Name | Rank in top 500 | Net worth | Club(s) |

| Bernard Arnault | 4 | $189B | Paris FC |

| Mark Mateschitz | 80 | $23.4B | Red Bull clubs |

| Stan Kroenke | 85 | $22.8B | Arsenal, Colorado Rapids |

| Philip Anschutz | 86 | $22.8B | Los Angeles Galaxy |

| David Tepper | 87 | $22.4B | Charlotte FC |

| Francois Pinault | 90 | $22.1B | Stade Rennais |

| Dietmar Hopp | 112 | $18.4B | 1899 Hoffenheim |

| Jim Ratcliffe | 200 | $12.4B | Man United, Nice, Lausanne |

| Hansjoerg Wyss | 218 | $11.9B | Chelsea, Strasbourg |

| Josh Harris | 224 | $11.7B | Crystal Palace |

| Simon Reuben | 227 | $11.5B | Newcastle United |

| David Reuben | 228 | $11.5B | Newcastle United |

| Dmitry Rybolovlev | 246 | $11.1B | AS Monaco |

| Mark Walter | 252 | $10.9B | Chelsea, Strasbourg |

| Dan Friedkin | 253 | $10.9B | AS Roma, AS Cannes, Everton |

| Shahid Khan | 307 | $9.33B | Fulham |

| Nassef Sawiris | 324 | $8.95B | Aston Villa, Vitoria |

| Daniel Kretinsky | 402 | $7.69B | West Ham, Sparta Prague |

| Joe Lewis | 405 | $7.66B | Tottenham |

| Todd Boehly | 426 | $7.28B | Chelsea FC, Strasbourg |

And the latest news illustrates exactly why the American billionaire has carved out that prestigious status.

Todd Boehly’s sports empire soars in value amid Clearlake rift

Boehly’s portfolio encompasses a number of different sports. He recently acquired a significant stake in London Spirit, a Hundred cricket franchise, for example.

But it’s on the other side of the Atlantic that Boehly’s biggest and most lucrative investments are found.

With fellow Chelsea investor Mark Walter, he owns a 27 per cent stake in NBA franchise the Los Angeles Lakers, as well as a 20 per cent stake in baseball’s 2024 World Series champions Los Angeles Dodgers.

The Dodgers had a magnificent 2024 and, thanks in part to the arrival of Japanese pitcher Shohei Otani – whose £550m, 10-year contract is one of the most lucrative in sports history – have skyrocketed in value.

Per a new ranking from industry experts Sportico, the Dodgers are now worth £6.5bn and have risen in value by a staggering 23 per cent in the last year alone, which was twice as fast as the next challenger.

They are also top of the pile in the revenue per game category.

And, at £6.5bn, the Dodgers’ worth has appreciated by 400 per cent since Walter and Boehly paid around £1.5bn to buy them back in 2012.

It’s the kind of record which will give critics pause for thought at Chelsea.

Stamford Bridge masterplan will dictate Chelsea’s future ownership

It has been over six months since a rift in the Chelsea boardroom was first reported, with stories at the time suggesting that it would eventually lead either Boehly or Eghbali to sell their shares.

The Chelsea Chronicle has been reporting for some time that the future of Stamford Bridge is one of the main differences between the two co-owners.

Now, Boehly has confirmed as much in his interview with Bloomberg.

“We have a big stadium development opportunity that we have to flesh out,” he told the financial outlet. “I think that’s going to be where we’re either aligned or we ultimately decide to go different ways.”

Boehly wants to take Chelsea to a new location at Earl’s Court, whereas Eghbali wants to remain on the existing site and expand Stamford Bridge.

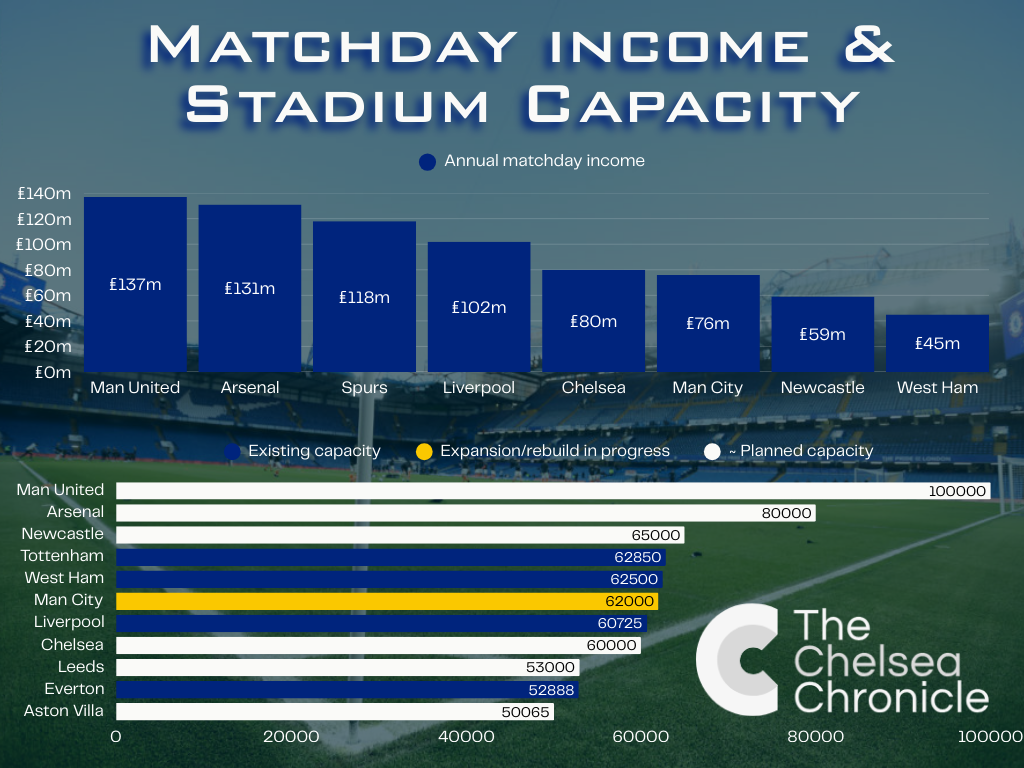

Either way, once the redevelopment or new stadium is complete, Chelsea will boast a capacity of over 60,000. In a Premier League marketplace increasingly focused on matchday income, that is just as well.

Chelsea earn more on a per-fan basis than every other Premier League club, but the relatively modest size of Stamford Bridge is limiting.

And with Manchester United set to build Europe’s biggest stadium, Liverpool, Manchester City and Spurs all having reached over 60,000, and Arsenal looking at a rebuild too, Chelsea can’t afford to stand still.

- READ MORE: Chelsea youngster breaks international record for youngest starter for his country in 2-0 win

Takeover latest: Could Todd Boehly flip Chelsea for a profit?

In the aforementioned Bloomberg interview, Boehly also insisted that Chelsea are worth more now than when the consortium he led paid £2.5bn for the club in May 2022.

Essentially, Boehly thinks he could make a profit if he was to sell Chelsea, or his stake in it, tomorrow.

“Has the enterprise value of Chelsea increased? Possibly,” says University of Liverpool football finance lecturer Kieran Maguire, speaking exclusively to The Chelsea Chronicle.

How Chelsea rank among sport’s most valuable teams

| Rank | Club | Value | 1-yr change | Owners |

| 17 | Manchester United | $6.2B | +4% | Glazer family |

| 18 | Real Madrid | $6.06B | +16% | Club members |

| 35 | FC Barcelona | $5.28B | +7% | Club members |

| 40 | Liverpool | $5.11B | +8% | Fenway Sports Group |

| 46 | Bayern Munich | $4.8B | +8% | Club members |

| 51 | Manchester City | $4.75B | +7% | Mansour bin Zayed Al Nahyan |

| 61 | Paris Saint-Germain | $4.05B | +19% | Qatar Sports Investment |

| 65 | Arsenal | $3.91B | +9% | Stan Kroenke |

| 74 | Tottenham Hotspur | $3.49B | +9% | Joe Lewis family trust, Daniel Levy |

| 75 | Chelsea | $3.47B | ±0% | Todd Boehley, Clearlake Capital |

“But that is to do with broader market issues as opposed to anything specifically to do with Chelsea.

“It’s a bit like saying ‘my house is run down but all the houses in the locality have gone up by 20 per cent, so I am riding somebody else’s wave.’

“So, I think it’s a little disingenuous of Todd Boehly to imply that it is his decision making that has contributed to the value.

“The enterprise value may have gone up. Enterprise value is the business assets part of the club balance sheets.

“If you then take away the debt element, it could be that the equity value of the club has decreased.

“So, there are ways of playing with numbers with regards to club value and this appears to be one of them.”

Receive a digest of our best Chelsea content each week direct to your mailbox